Reflecting the economic size and thereby the ability to repay debt, the fifth largest economy has been predominantly rated AAA. China and India are the only exceptions to this rule—China was rated A-/A2 in 2005 and now India is rated BBB-/Baa3.”

The Economic Survey further stated that changes in India’s sovereign ratings had a weak or no correlation with macroeconomic indicators and did not adversely impact yields on government securities, exchange rates and Sensex returns.

However, sovereign ratings can be pro-cyclical and could adversely affect foreign portfolio investment (FPI), both debt and equity, in developing countries.

Pro-cyclical, in this context, implies that credit rating agencies (CRAs) upgrade sovereign ratings during upswings and downgrade them during downturns. The latter practice exacerbates macroeconomic stresses.

Sovereign ratings don’t just affect FPI. The international credit ratings of public sector undertakings (PSUs) and public sector banks (PSBs) are linked to India’s sovereign ratings. The international credit ratings of PSUs and PSBs, among other factors, drive their foreign currency borrowing costs.

India’s sovereign ratings are constrained by its per capita income and fiscal deficit-induced indebtedness. How these metrics restrict sovereign ratings may be best understood by comparing India’s ratings and macroeconomic profile with the same of two developing Asian countries whose ratings were more or less at par with India’s a decade ago and have been upgraded since: Indonesia and the Philippines.

India’s 2023-24 fiscal deficit at 7.9% of GDP (overall) is more than thrice Indonesia’s and twice the Philippines’. The Indian government needs to improve India’s tax-to-GDP ratio. It should also mop up the excess liquidity of PSUs and sell non-core PSU assets to reduce fiscal deficits.

The government ought to emulate Singapore, which reports gross and net sovereign debt metrics. India’s gross-government-debt-to-GDP ratio at 86% in 2023-24 is higher than that of ‘BBB’ rated peers.

Also read: Mint Quick Edit | Will S&P upgrade India’s awkward credit rating?

However, if intra-government debt and the government’s liquid assets—the market value of its stakes in listed PSUs, the Employee Provident Fund Organization’s non-government investments and its deposits with the central bank—are deducted, the net-government-debt-to-GDP ratio moderates to about 61.5%.

While the onus of reducing its fiscal deficit and reporting gross and net sovereign debt is on the government, CRAs have overlooked India’s robustly growing GDP per head.

Historical disadvantage: A Moody’s note of 15 April 2024 stated, “India’s per capita income increased to about an estimated $8,300 on a purchasing power parity-adjusted basis in 2022 from around $4,900 in 2012, but remained the lowest among all investment-grade sovereigns.”

A Fitch note of 29 October 2024 observed, “Lagging structural metrics, including governance indicators and GDP per capita, also weigh on the rating.”

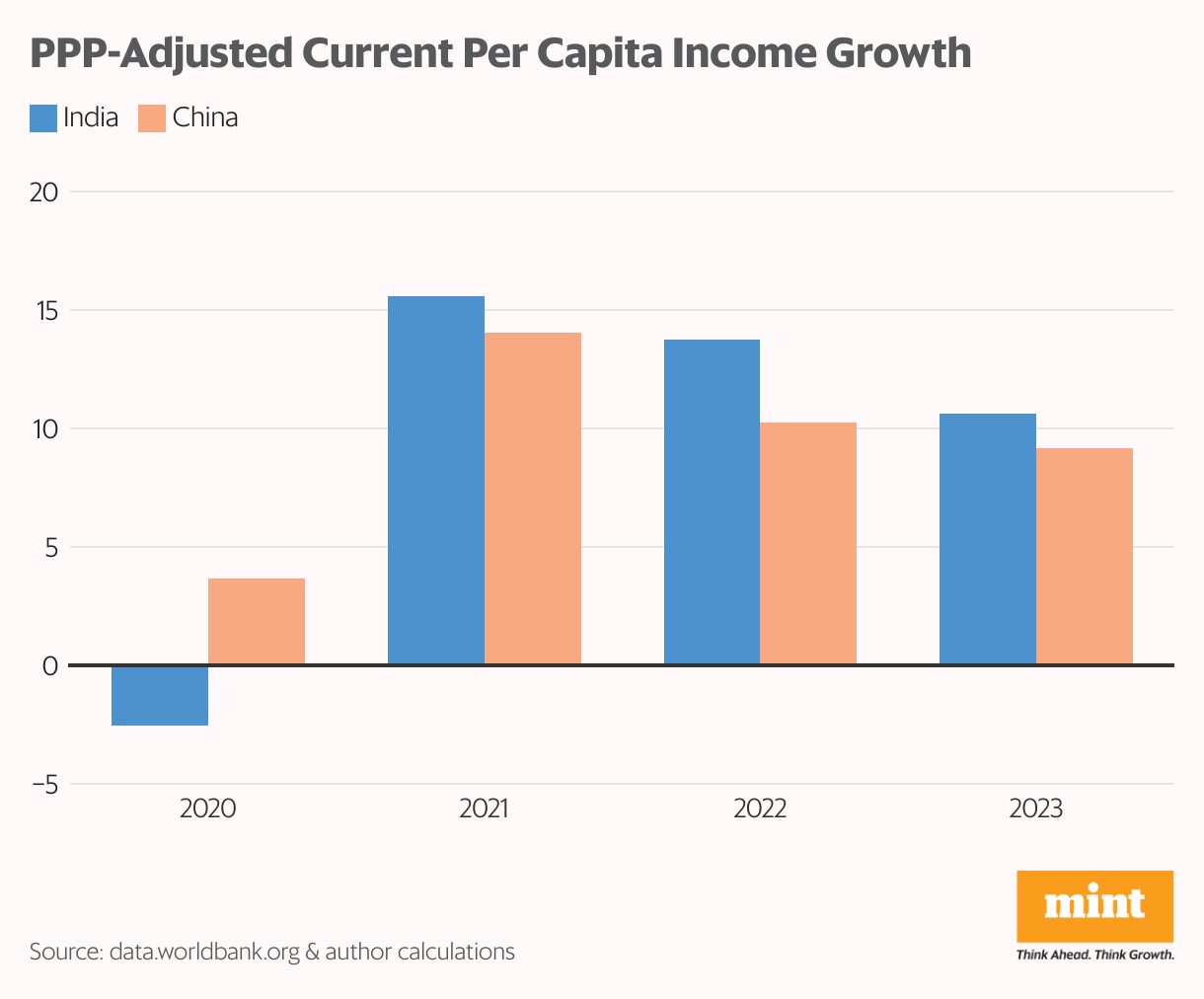

The World Bank estimates India’s 2022-23 GDP per capita at $2,485, which is marginally higher than the lower-middle-income country (LMI) average of $2,414. However, on a purchasing power parity (PPP) basis, India’s current GDP per capita is $10,176, almost 10% higher than LMI’s average of $9,308.

India’s PPP-adjusted current GDP per capita surpassed that of LMIs in 2017. In fact, India’s PPP-adjusted current GDP per capita has been among the world’s fastest growing since 1990, the first year for which the World Bank published this data.

The compounded annual growth rate (CAGR) of India’s PPP-adjusted current GDP per capita outstripped the figures of Indonesia and the Philippines, apart from low-income, LMI, middle-income, upper-middle-income and high-income countries for the 34-year period from 1990 to 2023 (see chart).

India’s PPP-adjusted current GDP per capita will exceed that of the Philippines by 2027 if both countries sustain their 2014-23 CAGR. The CAGR of India’s PPP-adjusted current GDP per capita has been at least 200 basis points higher than that of low-income nations since 1990, a sign that it is not just the small-base effect at work.

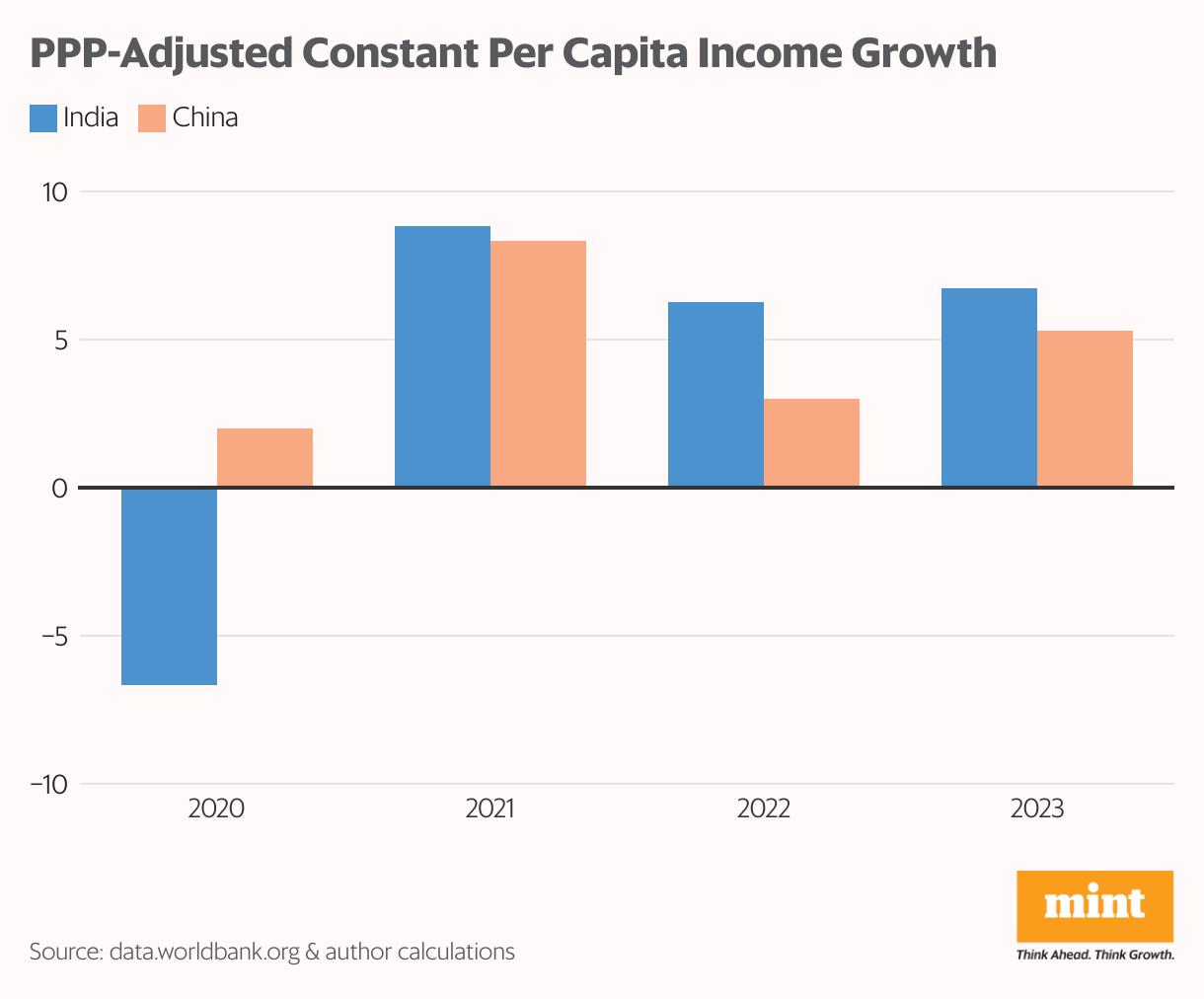

The results are identical when trends in PPP-adjusted constant GDP per capita, which excludes the impact of inflation, are analysed. India’s PPP-adjusted constant GDP per capita overtook that of LMIs in 2016, i.e., a year earlier than it did on a current basis.

The CAGR of China’s PPP-adjusted GDP per capita, both in current and constant dollar terms, has been higher than India’s between 1990 and 2023. However, year-on-year growth in India’s current and constant PPP-adjusted GDP per capita has been consistently higher than that of China’s since 2021 (see accompanying chart).

Global credit rating agencies have not incorporated in their assessments the outperformance of India’s PPP-adjusted GDP per capita, which, in conjunction with liberalization and improving governance, has created a virtuous cycle and is likely to be sustained.

While a country’s GDP per capita is an input for the sovereign credit rating models of Moody’s and Fitch, growth on this count is not. India is apparently being penalized for its historical though significantly improving low per-capita GDP.

Such sovereign credit rating methodologies work to the detriment of India and probably also other countries that were once colonized.

{kind=link}