Indian pharma companies have long been key providers of generic medicines to the US market, accounting for 47% of all generic prescriptions in 2022, according to a recent report by the IQVIA Institute.

But with growth in this business plateauting because of weaker demand, stiffer competition and expiring patents, companies are increasingly tapping the domestic market for branded medicines and health products, which has plenty of room to grow. Large, brand-dominated companies with numerous prescription drugs under their belt are poised to do well, as evidenced from the September quarter (Q2FY25) earnings so far.

Branded for growth

Mankind Pharma Ltd, which earns 91% of its revenue from its domestic business and has a prescriber penetration rate of almost 84% as of Q2, reported strong numbers for the quarter. Its chronic therapies – cardiovascular and anti-diabetic medicines – outperformed the overall domestic pharma market, driving 10% on-year growth in its Indian branded prescription business.

Sun Pharmaceutical Industries Ltd also saw strong traction for its prescribed branded medicines, leading to 11% on-year growth in its domestic business despite its large size. With a market share of around 8%, Sun Pharma is the largest pharma company in India. It launched 14 new branded products in Q2 alone and has 28 branded products among India’s top 300 brands.

“On the branded side, larger companies often clock higher growth because consumers tend to stick to the brand mentioned in the prescription,” Prashant Nair, director at Ambit Capital, told Mint. “Hence brand-heavy stocks always sell at a premium.”

Also read | Sun Pharma: Down but not out?

Brand recall is key for the consumer healthcare segment as well. Mankind’s consumer healthcare business grew 20% on-year owing to robust demand for brands such as Manforce, Gas-o-fast and HealthOk. While Mankind’s strong brand recall buoyed over-the-counter (OTC) sales, quick-commerce channels further boosted sales of such branded products, raising Mankind’s Ebitda margin by 400 basis points sequentially to 27.3% in Q2.

Cipla’s consumer healthcare business also grew 21% on-year and the company plans to increase the revenue share from this segment from 8-9% at present to 15% in the long term. However, OTC and prescription sales of Cipla’s branded products underperformed in Q2, owing to lower demand for its acute therapies such as cough and cold medicines, and anti-infectants.

g-Revlimid to drive US slowdown

The slowdown in the US is expected to be driven by falling sales of generic versions of Revlimid (g-Revlimid), a drug used to treat certain types of cancer. These drugs account for a huge portion of US generics sales for Indian pharma companies, but after a blockbuster three-year run, incremental gains from sales of g-Revlimid are expected to slow down in the next couple of years, ushering in a cyclical slowdown in the US generic drug market.

Generics-heavy companies are already starting to feel the effects of this. Cipla’s US business languished in Q2 owing to 5% lower sequential sales of g-Revlimid, while Biocon’s US generics sales fell 8% on-year in Q2. That said, Cipla, Biocon, Dr. Reddy’s Laboratories and Sun Pharma, among other copycats, still reported healthy contributions from Revlimid generics in Q2 as it is a high-margin product.

Also read | A prescription for speed: How e-pharmacies aim to transform medicine delivery

“While we acknowledge [Dr Reddy’s] R&D efforts, we believe these will still not be enough to fill the g-Revlimid void,” said an Incred Equities report on the company’s Q2 earnings. “Dr. Reddy’s runs high earnings concentration risk but will have a strong near-term earnings trajectory while the strong contribution from g-Revlimid prevails until Q3FY26.”

Nomura had a similar view of Cipla, saying revenue contribution from g-Revlimid will be insignificant in FY27 owing to stiffer competition. While some drug patents are due to expire in the next couple of years, analysts expect generic anti-obesity and anti-diabetic GLP-1 drugs to be the major catalyst for the next upswing in the generics business. But Normura believes Indian players are likely to fully reap the benefits of GLP-1 drugs only towards the end of the decade.

Taking stock

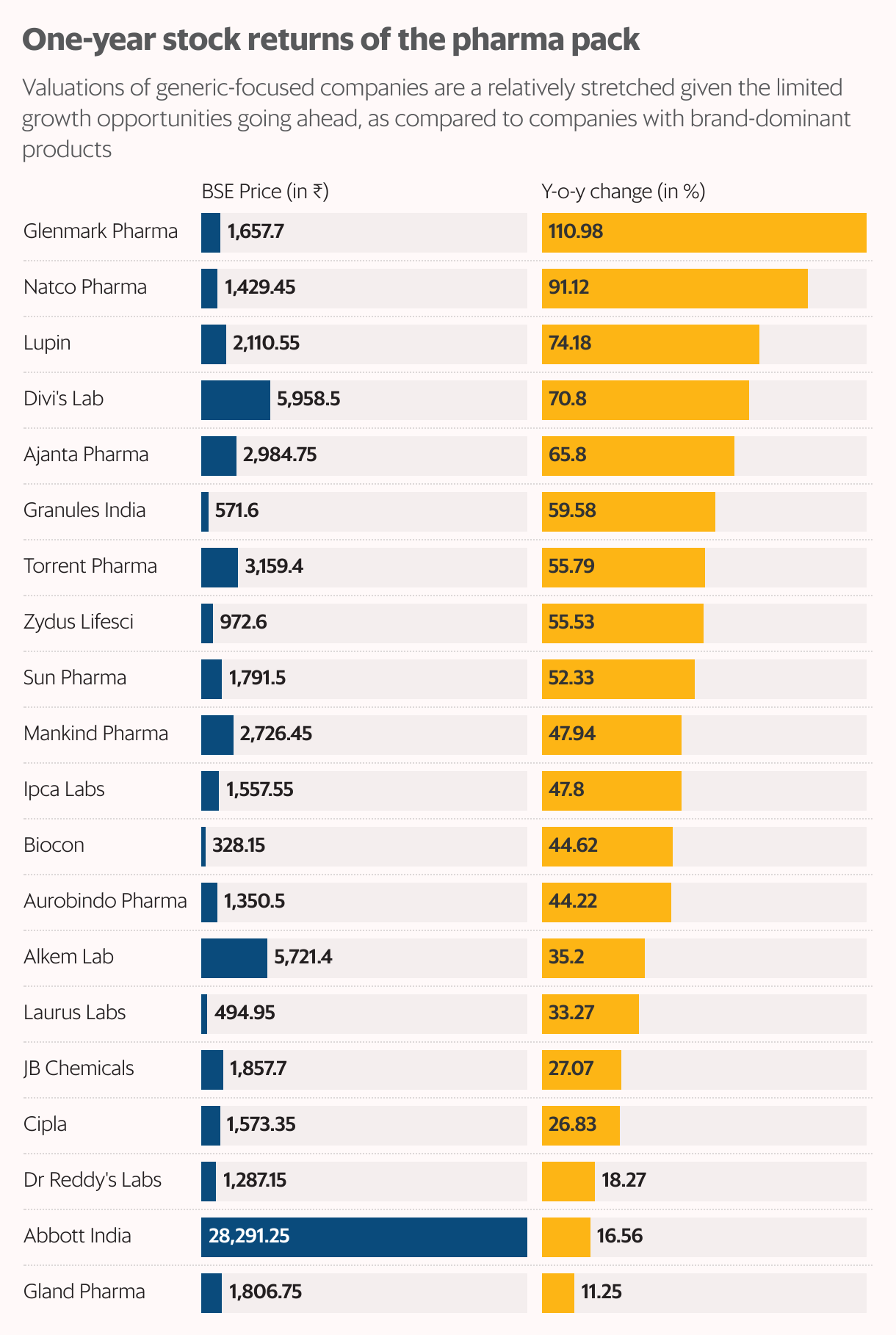

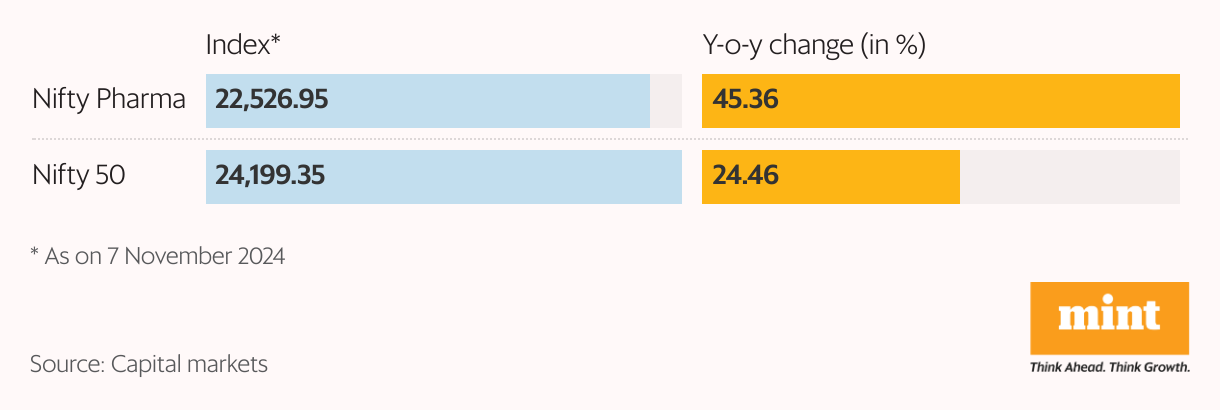

Until then, brand-heavy companies are better positioned to justify their current valuations, with the stocks of Mankind Pharma, Sun Pharma, Torrent Pharmaceuticals and Eris Lifesciences returning 50% on average in the past year. On the other hand, generics-focused Cipla and Dr. Reddy’s returned only 26% and 18% respectively over the same period, underperforming the Nifty Pharma index’s return of 45%.

Also read: ‘Laddus’ to drugs, adulteration is a national crisis

“For generics, the best of the cycle has played out and a slowdown will start soon. Hence brand-dominant companies are currently offering better value, given the growth opportunities,” said Ambit Capital’s Nair. “The branded business is always superior to the generics business and countries like India have more room for it to grow.”

{kind=link}